The epiphany tripped me up like that unseen root on a mountain trail run that sends you tumbling. For a few surreal seconds, time seemed to slow and I found myself asking: when did this happen? Why was it not obvious to me before? What had changed?

In disbelief, I saw it all clearly, as if for the very first time. Technology. Empathy. Putting the person at the centre of the design. And, perhaps most importantly, asking, “why, why, why?”

It was my ‘aha’ moment, as I sat in a health tech accelerator in Chicago. Surrounded by my professors from Kellogg School of Management, together with an array of entrepreneurs, designers, innovators and executives from Ideo, the legendary design and innovation consultancy who are the thought leaders behind human-centered design, and Doblin, the authors of “Ten Types of Innovation”, I began to see technology in a whole new light.

Technology was no longer scary, a novelty, or clunky. Rather, I saw it as a tool for solving real-world problems in unique ways. Cloud computing, artificial intelligence, open application programming interfaces (or APIs, which basically allow different applications to talk to one another), web-based tools, scalable servers, low-cost smart handsets – these technologies have levelled the playing field. Barriers to entry, to innovation, to solving problems, have radically shifted.

Another aha moment

My experience in Chicago was the first in a journey towards a greater understanding of our technological landscape. Recently, at the Singularity Summit in Johannesburg, I had another one of those ‘aha’ moments. For those unfamiliar with Singularity University (SU), the organisation explores the scope for exponential technology to solve some of the world’s most urgent problems. (If you are interested in diving a bit deeper, I suggest you read “Abundance” and “Bold”, penned by SU’s founders, Peter Diamandis and Steven Kotler.)

At the summit, it was Richard Browning, an inventor, who discussed how exponential technologies have shifted from “unready to hand” to “ready to hand”, highlighting the momentous manner in which this shift is impacting humanity. Of course, this makes sense when one applies the notion of “ready to hand” to technology, where this phrase means something which is easily accessible or readily available. On the other hand, technology which serves a purpose but does not fit seamlessly into everyday life, rather requiring a special effort of some sort, would be considered “unready to hand”.

When a new technology initially arrives, it is usually “unready to hand” – although more than ready to be adopted by early innovators. Such technological buffs ‘de-risk’ the technology to the point where early adopters take greater interest. Gradually, it is refined, with functionality being better understood, limitations acknowledged and future potential progressively unlocked.

Shifting from “unready” to “ready”

A case in point is the evolution of digital mapping technology. Perhaps few can recall, but Google Earth was acquired and developed by Google four years prior to Google Maps. Google Earth possessed a novelty which appealed to curious explorers and, of course, those who enjoyed zooming in on their homes to spy on their dog in the yard. It showcased the ubiquitous nature of technology, but it was still “unready to hand”, lacking in everyday appeal.

The salient point: one could not exactly open up Google Earth and find the fastest route to the airport. A lighter, more user-friendly tool was required. Queue Google Maps. Once Google went on to make the technology available as an easy-to-use service (or API), it ignited exponential innovation from the likes of Uber, Airbnb, OrderIn, Waze, Taxify, geo-fenced marketing campaigns, location-based KYC – you name it. Google Earth is “unready to hand”, while Google Maps is “ready to hand” – a part of everyday life. Think about it this way: when last did you ask anyone for directions, where the response went something like, “So, you turn right at the traffic lights and then after one kilometre, turn left…”?

Wealth management technology

The same logic is being applied to wealth management, where there is a tectonic shift underway. Investment platforms have historically built their value proposition around the ability for bulk trading, offering a decent selection of product options in a single place, and providing basic reporting. In practice, the experience for the adviser is that of an “unready to hand” technology. Trades are limited to certain days due to fee or debit order batch runs, or some other restrictive process. Corrections are frequent. Manually entering information results in unnecessary errors and poor client experiences. An adviser’s day-to-day work experience has to fit into a platform’s severe limitations.

One has to ask, “why?”

Why can a platform not fit seamlessly into the adviser’s daily operations? What’s more, why can a platform not remove complexity, prioritise the experience and improve the client’s understanding and outcomes, rather than focusing purely on efficiency and choice. Surely, this should exist?

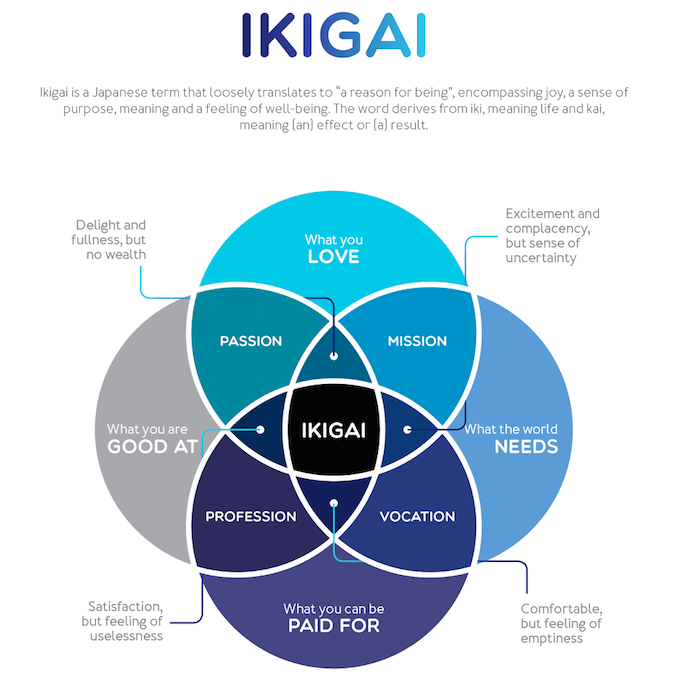

Our Ikigai

The good news is that it’s INN8’s vision to do just this. At INN8, we live by the mantra of “changing the way investments are done” by designing our platform to be “ready to hand” for advisers and their clients. We do this by putting the adviser and client at the centre of everything we design. It’s not an easy process, but it’s our ‘Ikigai’, our reason for being.

If you are an adviser looking to future-proof your business and delight your clients using “ready to hand” technology, then INN8 is the partner for you. If not INN8, then who?