Key person risk is one of the most important non-financial risks faced by investment management businesses.

Key person risk is one of the most important non-financial risks faced by investment management businesses. It refers to the dependence of an investment strategy, process or organisation on one or a few individuals whose absence would materially impair performance, continuity or stability. While widely understood conceptually, in practice it is often underestimated.

Most investors recognise the concept, but the bigger challenge is when it becomes a real problem. In practice, it is often reduced to a name on a factsheet, a founder-led reputation; or a clause in a due diligence questionnaire. The more relevant question is not whether certain individuals matter, they always do, but whether the organisation can continue to operate effectively without them. That is often when key-person risk moves quietly from theory into reality.

In this article we briefly unpack key-person risk and our preference for team-based decision-making.

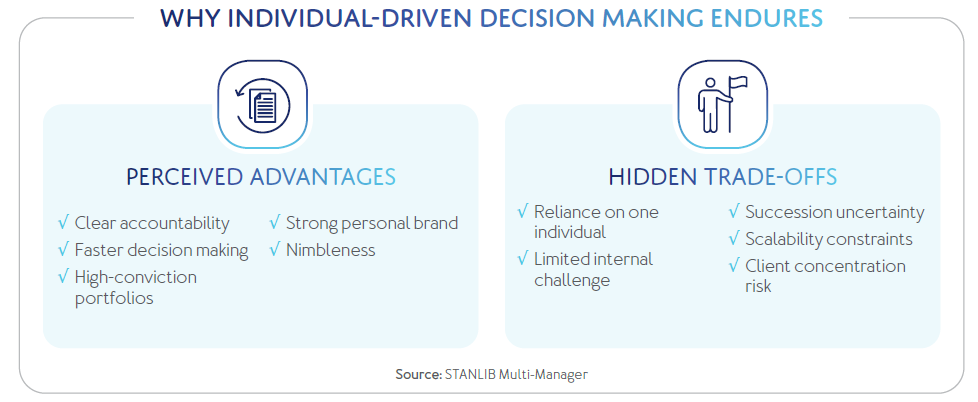

Despite the industry’s broader shift towards team-based investment decision making, individually driven decisions remain common. In some firms, especially boutiques, this reflects genuine concentration of experience, judgement or specialist capability in a founder or lead portfolio manager. We recognise that this clear accountability could be attractive to investors.

However, it is more common to find individual-driven decision making in investment processes that are style driven where a particular individual’s skill and experience are drivers of performance and the reputation of the asset manager is linked to that individual - the so-called ‘star manager.’ While this approach can offer advantages, it also introduces several tradeoffs as outlined below.

We also want to highlight that key-person risk is not only about a star portfolio manager. It can also arise around senior analysts, sector specialists, quants, operational leaders or anyone else who holds non-substitutable intellectual capital, tacit workflows, proprietary frameworks, decision rights or key client relationships.

Key-person risk becomes material when the supporting structure is not strong enough to absorb change and disruption.This can arise where:

We have seen this play out in different ways. In one example, an experienced fixed-income manager with a strong performance record left a business that appeared to have managed succession sensibly on paper. A structured handover took place with another respected industry figure being appointed. Yet client outflows occurred. The episode highlighted that even where process appears robust, perception can amplify dependency if clients are anchored as much to the individual as they are to the strategy.

In another example, a boutique equity capability faced an unexpected sabbatical from a co-founder and lead portfolio manager who had played a central role in shaping the team’s philosophy, relationships and strategic evolution. While we were initially concerned, succession planning had already been tested, the co-portfolio manager structure was active, communication stressed continuity and clients could see credible depth in the team. Stability returned relatively quickly and outflows were limited.

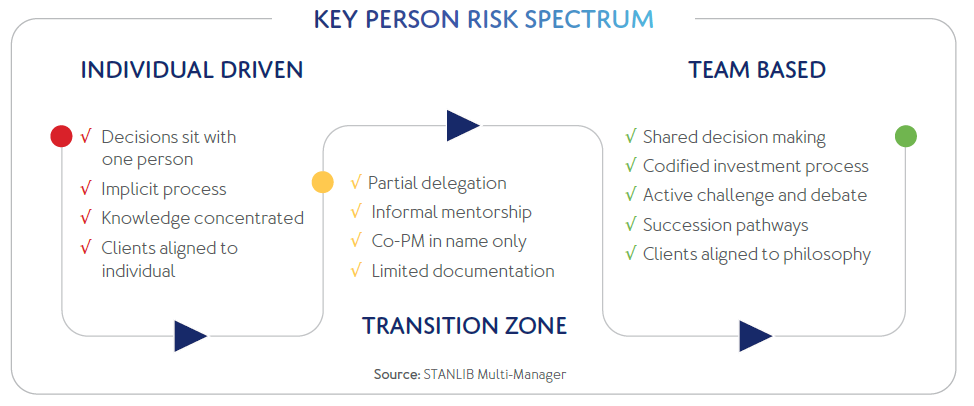

Both situations involved pressure. The difference was not the absence of strong individuals, but rather the resilience that was already embedded in the organisation. In practice, organisations can sit on a spectrum of dependency and resilience - from individual driven to team-based - as outlined below.

Assessing resilience requires moving beyond structures and titles to understand how decisions are actually made. The central question is straight forward: can the investment process continue to deliver consistent outcomes if any one individual steps away?

Where the answer is yes, decision making is likely institutionalised. Where the answer is no, the organisation remains exposed. Since team size and titles do not tell the full story, we evaluate resilience by asking several fundamental questions:

Ultimately, the question is not who matters, but whether the organisation retains its identity when an individual steps away. Critically, resilience is not just about having a large team. It depends on whether the team members bring independent perspectives. A group that converges too easily may still reflect a single viewpoint, leaving blind spots intact.

Our preference for team-based investing is practical, not ideological. It is a risk-management tool. Strong leaders and exceptional individuals still matter, and a team-based structure should not dilute accountability or conviction. Long-term success should never depend excessively on any one person.

When properly structured, teams create resilience. They embed challenge and debate, reduce behavioural bias, support continuity and make it less likely that the success of a strategy depends on an individual’s continued presence, energy or judgement. That does not weaken strong leaders - it strengthens them by surrounding vision and accountability with depth, continuity and independent perspectives.

Ultimately, the question is not whether one person is talented or influential. It is whether the organisation retains its identity, discipline and philosophy when that person steps back. That is what we believe matters most.

Resilience is not the absence of star talent; it is the ability of an organisation to deliver its philosophy when the stars are off the stage. Moving beyond dependence on individuals and embedding judgement is what makes an investment business more robust, sustainable and better positioned for the long term.