Financial advisers and intermediaries have embraced several challenges over the past couple of years, from Covid-19 to an onerous regulatory environment.

Financial advisers and intermediaries have embraced several challenges over the past couple of years, from Covid-19 to an onerous regulatory environment. And it is not getting easier as we prepare for the next wave of regulatory reform – the Conduct of Financial Institutions Bill (CoFI). The proposed Bill promises a significant shake-up for South Africa’s financial landscape and financial advisers stand at the epicentre.

While the ultimate impact remains to be seen, understanding the potential implications and exploring mitigation strategies is crucial for navigating the future successfully. In this article, we briefly touch on the ramifications for financial advisers and how DFMs may help to navigate these regulatory hurdles.

What is the purpose of CoFI?

When promulgated, the CoFI Bill will become the CoFI Act and will replace the FAIS Act together with many other pieces of financial services legislation, with the sole purpose of protecting customers. All in all, it aims to deliver better customer outcomes in the financial sector, with a strong focus on fairness and transparency.

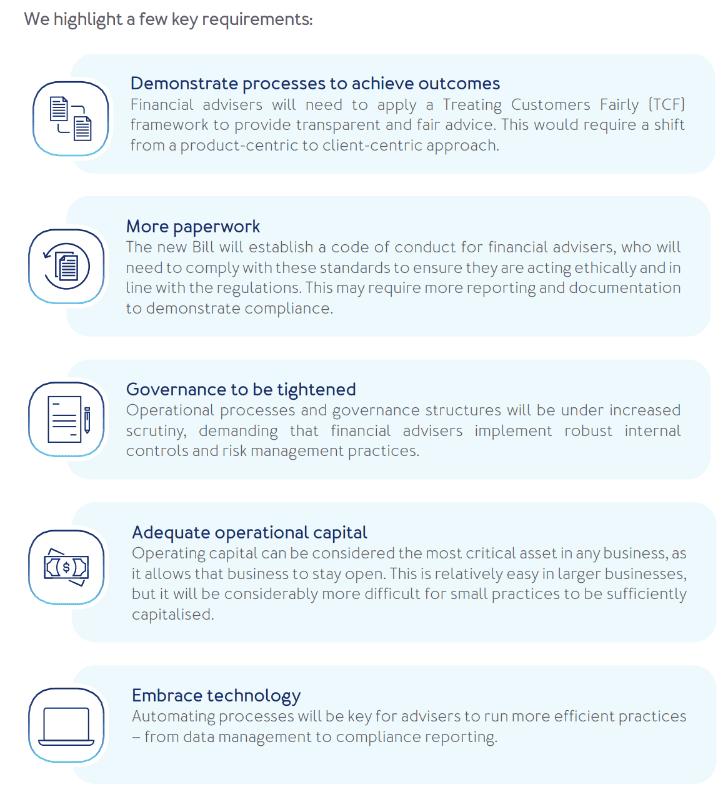

CoFI will therefore force Key Individuals to take a step back and re-evaluate current business philosophies, business cultures and processes. The CoFI Bill aims to move away from a reliance on detailed, prescriptive rules, instead relying on broadly stated rules or PRINCIPLES to set the standards by which financial institutions must conduct their business.

Therefore, once the CoFI Bill is enacted, financial institutions will no longer simply be ticking requirements off a list. Rather, they will have to seek different ways in which they can be more customer focused. A principles-based approach does, however, not entail an absence of rules or detailed requirements. The Financial Sector Conduct Authority (FSCA) will be empowered to issue conduct standards through the CoFI Act, setting out specific binding requirements that financial advisers will need to adhere to.

Financial advisers put to the test

The capacity of financial advisers has already been stretched beyond the limit. After facing a perfect storm for many years, advisers are now facing the challenges that the new law will require from them. Fortunately, the implementation of the required legislation will take place in various stages over the next few years, allowing advisers to gradually bring their practices in line with the new legislation.

A reputable DFM may be the answer…why?

Partnering with the right DFM presents a strategic opportunity for those advisers who can adapt and plan to form partnerships under the new legislation. Some of the added benefits of this approach are discussed below:

Conclusion

Overall, the CoFI Bill seeks to create a more transparent, fair, and accountable financial advice industry. Financial advisers will need to ensure they understand and comply with all the new regulations. The Bill presents many challenges for financial advisers, but also opportunities. Partnering with a DFM can be a strategic decision to overcome many of the regulatory complexities, achieve operational efficiency and enhance the client experience.

At the time of writing this article, National Treasury intended to submit the Bill to Parliament in the latter part of 2024.