In the first of an updated three-part series, we discuss how you can save on tax by starting to contribute – or contributing more – to your current retirement fund(s). The updated series focuses on section 11F of the Income Tax Act – the deduction of contributions to retirement funds.

Remember that all contributions towards retirement funds are tax deductible in terms of Section 11F of the Income Tax Act. As the tax year-end approaches on 28 February 2023, you can benefit from a tax deduction when filing your tax return for the year of assessment.

The amount of the deduction in a particular year of assessment is limited by Section 11F to the lesser (smaller) of A, B, and C below:

A: R350 000

B: 27.5% of the greater of:

Remuneration, excluding retirement lump sum benefits and severance benefits; or Taxable income including a taxable capital gain but before allowing this deduction and the section 18A donations deduction. It also excludes any retirement lump sum benefits and severance benefits.

C: Taxable income before the section 11F deduction and before the inclusion of the taxable capital gains

Any contribution over (the smaller of A, B, and C above) that does not qualify as a deduction in the year of assessment, will be carried forward to future years of assessment, subject to the annual limit.

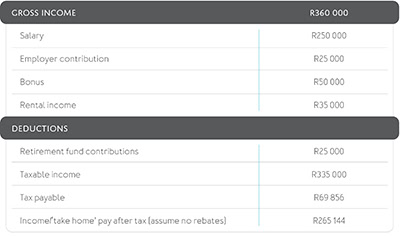

The maximum deduction that Mrs Selinda can make is limited to the lesser of the:

A: R350 000

B: The greater of:27.5% x R325 000 (remuneration) = R89 375or 27.5% x R360 000 (taxable income) = R99 000

C: R360 000 (taxable income) - R0 (no taxable capital gain) = R360 000The deduction will be limited to the lesser of the three amounts in bold, which is R99 000.

Mrs Selinda only contributed R25 000 and can therefore deduct the full amount of R25 000 for tax purposes.

In the example above, for every R1 invested (retirement fund contributions) by Mrs Selinda, SARS will provide tax relief and ‘refund’ her with not less than 30 cents. Her R25 000 annual contribution effectively resulted in a tax saving of R7 558 p.a.

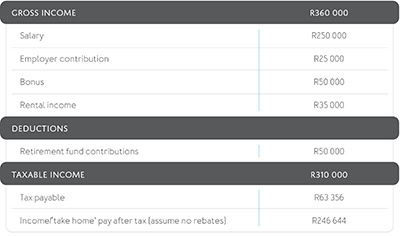

Example 2: Tax saving when increasing contribution

The maximum deduction that Mrs Selinda can make is limited to the lesser of the:

A: R350 000

B: The greater of: 27.5% x R325 000 (remuneration) = R89 375 or 27.5% x R360 000 (taxable income) = R99 000

C: R360 000 (taxable income) - R0 (no taxable capital gain) = R360 000

The deduction will be limited to the lesser of the three amounts in bold, which is R99 000. Mrs Selinda contributed R50 000 and can therefore still deduct the full amount of R50 000 for tax purposes.

Although Mrs Selinda’s contribution doubled from R25 000 to R50 000 per annum, her take-home pay only dropped by R35 942 per annum (from R282 586 to R246 644). This resulted in overall tax relief of R14 058 per annum.

Mrs Selinda had the option to increase her contribution (refer to example 2) within her occupational fund (pension fund) and/or via a retirement annuity (RA). She opted to contribute towards both retirement vehicles. The main reasons for this are:

The law states that it is not possible to withdraw from an RA other than when you have reached 55 years of age; the fund value is less than R15 000; on permanent disability; or if you have been a non-resident for South African tax purposes for a period of three consecutive years on or after 1 March 2021. Hence, if you are thinking of emigrating, you may have to think twice before investing in an RA as you will need to wait three years before you are able to access that money.

¹ Any contribution amount to a retirement fund that was not income tax deductible in the year it was made will be property in the deceased estate. This will be for all deaths occurring on or after 1 January 2016 and for all nondeductible contributions to retirement funds made on or after 1 March 2015.

South Africa has several tax initiatives to encourage a savings culture. You should consider taking full advantage of the current legislation if you wish to save more toward retirement. In addition to the annual tax-free amount of R36 000 in an appropriate tax-free savings account, making additional contributions towards retirement savings is a no-brainer.