Markets shifted from anticipating rate cuts to pricing in rate hikes, as an energy supply shock and geopolitical risk reshaped the inflation outlook in Q2.

The United States and Iran announced an interim peace agreement in June, easing concerns over a conflict that has weighed on economic sentiment and energy markets for more than three months. The 14-point memorandum opens a 60-day negotiation period during which Iran will allow toll-free passage through the Strait of Hormuz, a key oil and gas shipping lane. The preliminary accord defers many of the more difficult issues such as Iran's nuclear program.

Global equity markets ended the quarter higher despite the geopolitical challenges and inflation concerns. The MSCI AC World Index delivered another impressive quarter with a double digit return of 14.9% in US dollar terms. Global equity performance has become much more diversified. Attribution shows that US artificial intelligence (AI) is still the engine but Europe, Japan and Asian semiconductor markets - such as South Korea and Taiwan - have become important contributors. Chinese equities edged toward a bear market as sentiment soured on tepid consumer spending and fading confidence in e-commerce companies. Global bonds underperformed equities mainly due to higher yields, large fiscal deficits and renewed rate-hike fears. The Bloomberg Global Aggregate Index returned only 0.8% in Q2.

On the macro-economic front, markets experienced a significant shift in interest rate expectations. The energy supply shock is complicating the inflation outlook for central banks worldwide. At the start of the year, investors anticipated multiple interest rate cuts from most major central banks. Governments responded by reversing course on monetary easing and the European Central Bank (ECB) became the first major central bank to raise rates - its first hike since 2023. The widely anticipated decision reflects growing concern over renewed inflationary pressures. Emerging market central banks are also tightening policy to support their currencies and stem capital outflows. Since the war commenced in late February, at least ten emerging and frontier markets - from Indonesia and Sri Lanka to South Africa - have raised interest rates.

The US/Iran ceasefire lowers future inflation risks but does not reverse the inflation that has already occurred. It will take time to restore production capacity, repair infrastructure and get ships sailing again and in the meantime, efforts to rebuild inventories will keep crude prices elevated. Markets are not yet convinced the inflation threat has disappeared and are still pricing a 'higher-for-longer' interest rate environment rather than a return to the rate-cutting cycle that investors expected earlier in the year. By way of an example, the US Fed did not raise rates in June but has become markedly more hawkish.

Kevin Warsh's first meeting as head of the Federal Reserve (Fed) marked a distinctive break from how the central bank operated under Jerome Powell. Among the changes: a much shorter policy statement and five new task forces that could reshape the Fed. The Fed decided to leave the Federal Funds Target Interest Rate unchanged at a range of 3.50% to 3.75% but the interest-rate projections had a sharp pivot toward raising rates. The Fed's forward-looking dot plot swung abruptly - nine Fed officials now project at least one rate increase this year.

This did not come as a surprise, due to stronger GDP growth, the May employment report and Personal Consumption Expenditures Index (PCE) that increased 4.1% y-on-y and breaking above 4% for the first time in three years. The PCE index is the Fed's primary benchmark for assessing inflation and tracking its 2% annual target. The persistent price pressures could encourage the Fed to maintain their restrictive monetary policy for a lot longer.

The artificial intelligence boom has sparked a massive rally for chip stocks, netting a record for the widely followed PHLX Semiconductor Index, which gained 88% in Q2. This despite a late tech sell-off with renewed scepticism as to whether AI companies will deliver profits that justify the billions of dollars being spent.

Demand is surging across almost every category of chips, from the more basic CPUs that companies such as Intel, Arm Holding and AMD specialise in, to the AI accelerators, or GPUs, made by Nvidia, to the memory chips that allow servers to store the caches of data required to operate AI models. In view of that, the gains of chip shares have been extraordinary. Sandisk has soared more than 700% this year, Intel has more than tripled and Micron has climbed into the ranks of $1 trillion companies. The company's share has been on a tear, climbing 240% this year and a staggering 850% over the past 12 months. The S&P 500 Index was up 15% in Q2 and 10% YTD. The Nasdaq Composite, that now includes SpaceX, jumped 21% in Q2, up 13% YTD.

SK Hynix is a South Korean multinational semiconductor company and a pioneer in the AI hardware ecosystem. SK Hynix is the primary supplier of High Bandwidth Memory (HBM) to tech giants like Nvidia, whose GPUs cannot function effectively without HBM memory chips stacked alongside them. Therefore, Nvidia is a major client and partner for those HBM products supplied by SK Hynix and their direct competitors - Samsung and Micron. Though SK Hynix still has an edge in that market, Micron have raced to catch up in recent years. Micron and SK Hynix made back-to-back announcements of late that solidify the memory chip market as the hottest part of the AI industry. Micron delivered sales and profit forecasts that shattered analyst estimates, while SK Hynix disclosed plans for a blockbuster listing in the US.

Goldman Sachs said strong corporate earnings and resilient consumer spending indicate the US economy remains on a solid footing, although slowing household demand and rising cost pressures could weigh on growth later this year. Corporate earnings during the first quarter exceeded expectations across much of the S&P 500. Consumer spending has also remained stronger than many investors anticipated. The overall earnings picture remains strong with total Q2 earnings for the S&P 500 Index currently expected to be up 22% on 10% higher revenues y-on-y, according to Zacks Investment Research. Looking at the calendar year picture, Wall Street analysts project S&P 500 earnings to grow between 21% and 24% for the full calendar year, driven heavily by an unprecedented wave of upward revisions and investments in artificial intelligence.

Space Exploration Technologies Corp (SpaceX) became the largest IPO in history, shattering the previous IPO fundraising record held by Saudi Aramco of $25.6 billion in 2019. SpaceX shares surged in their first day of trading in June following a record breaking $75 billion IPO that was more than four times oversubscribed by institutional and retail investors. The IPO set the stage for large offerings from OpenAI and Anthropic later this year, having raised money in the private markets at $852 billion and $965 billion, respectively. All three would end up being larger than any IPO ever recorded by all measures. However, OpenAI is reportedly considering delaying the timing of its IPO until next year.

Apart from the valuation challenge - SpaceX, OpenAI and Anthropic are all currently not profitable - they also create a challenge for passive investing and benchmarks. But why?

The S&P Dow Jones Indices have decided to maintain existing eligibility requirements for major benchmarks such as the S&P 500 Index, including the 12-month seasoning period and existing profitability and public-float requirements. It is for this reason that SpaceX will not be eligible for S&P 500 inclusion until at least mid-2027. By contrast, other major index providers, such as the FTSE Russell, Nasdaq and MSCI, are moving more quickly to include very large IPOs. Because SpaceX's free float - the percentage of shares available for public trading - is relatively small compared to its massive valuation, its weighting in the MSCI World index is expected to remain small, less than 1%. J.P. Morgan estimated that SpaceX's inclusion in the Nasdaq 100 could draw $4.3 billion in passive inflows.

Differing fast-entry rules across index providers may create a period in which active managers can add or lose significant value through out-of-benchmark exposures, while passive investors may experience unexpected performance differences if their portfolio implementation and reference benchmark are not aligned.

Chinese growth was up a robust 5.0% y/y in Q1 2026 - still clearly 'export-led' with consumer spending a drag on overall growth. In May, China recorded another strong trade balance. The acceleration in the trade surplus was boosted by a surge in exports, led by a strong acceleration in shipments of high-tech products, while imports fell for the first time since October 2025.

China's headline consumer inflation rate remained unchanged at 1.2% y/y in May, suggesting that the weak domestic demand conditions are preventing higher producer prices being passed through to the consumer. China's headline inflation rate has been below the People's Bank of China's (PBoC) implicit target of 2.0% for more than three years. Accordingly, the PBOC left interest rates unchanged. The rates have been held steady for 13 consecutive months.

The equity market had a tough period. The MSCI China Index ($) dropped 15% YTD. The sell-off was primarily driven by weak domestic consumption and disappointing performance in heavyweight tech shares. The technology exposure in the index is more concentrated in e-commerce and internet platforms and lacks significant exposure to global hardware and AI supply chains, which shot the lights out. Major constituents like Alibaba and Tencent Holdings Ltd posted March-quarter revenues that missed analyst expectations.

Japan's economy grew at an annualised rate of 2.1% in Q1, beating expectations. The Bank of Japan raised its policy interest rate by 0.25% to 1%, the highest level since 1995. The country has finally moved out of the long era of deflation (falling prices) and now faces more persistent inflation pressures and gradually returning monetary policy to normal. For decades, Japan struggled with weak growth and very low inflation. However, prices have been rising more consistently with companies granting larger wage increases and higher global energy prices. Lastly, while a persistently weak yen helps boost corporate profits by making it easier for manufacturers to export goods produced domestically, it increases the burden for companies and households through higher import costs, adding to inflation. Fortunately, Japan's annual core inflation stayed below the central bank's 2% target for a fourth straight month in May.

The equity market surged ahead with the Nikkei 225 Index up an astonishing 37% in Q2, driven by a combination of AI enthusiasm, a weak yen and renewed international investor demand for Japanese equities. Large index constituents such as Advantest, Tokyo Electron and Kioxia have risen sharply because they supply equipment, infrastructure and capital to the global semiconductor industry. Kioxia, which specialises in unglamorous flash storage that has also seen an AI-driven surge in demand, is up close to 700% this year and now Japan's most valuable company. Kioxia was spun out from scandal-ridden Toshiba Corp. in 2019 and then had its public debut delayed multiple times due to lacklustre investor demand.

Eurozone inflation quickened as the Middle East war strained supply lines. CPI rose to 3.2% in May, up from 3% in April and overshooting the ECB's medium-term target of 2%. The ECB subsequently raised interest rates by 0.25% to 2.25% in June. The Bank of England kept its base interest rate steady at 3.75% and acknowledged that it was "hard to predict" what will happen to prices because of the Iran war. Annual inflation in the UK was unchanged at 2.8% in May and the economic backdrop remains weak.

European markets have broadly trailed Wall Street and Asian benchmarks this quarter, primarily due to a lower concentration of major technology shares. Still, the STOXX 600 Index was up a 'healthy' 10% for the year. Performance has been relatively broad-based, led by financials, specifically banks.

The local economy achieved an encouraging 1.9% y/y growth rate in Q1, up from 0.8% in Q4 2025, driven by strong performances in the agriculture and finance sectors. Unfortunately, despite better growth numbers, the SARB had to raise interest rates in Q2 after headline inflation accelerated to 4.5% y/y in May from 4.0% in April, on the back of the large petrol increases triggered by the war in the Middle East. Also, of concern is the trend in fixed investment, which hovers below 14% of GDP, falling significantly below the roughly 25% of GDP needed to support growth of 3% or higher.

Fitch Ratings upgraded South Africa’s long-term sovereign credit rating to BB from BB-, while maintaining a stable outlook. This marks Fitch’s first upgrade in nearly 21 years, signalling growing confidence in the country’s fiscal management despiteremaining in sub-investment grade territory.

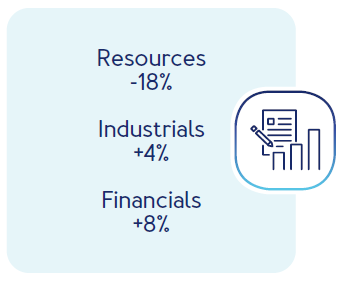

It has been a challenging quarter for the local equity market. The JSE All Share Index lost 2.4% in Q2 and 3% YTD. The market was dragged down by gold and PMG shares. Resources were down 8.6% but industrials and financials were up 4% and 8%, respectively.

Over the past six months large, diversified mining companies like Anglos and BHP have generally outperformed single-commodity miners. The main reason has been their multiple earnings drivers that include copper, which has been one of the best-performing industrial metals due to accelerating investment in AI-related data centres. Strong gold and platinum group metal (PGM) prices delivered much of last year's returns. But we know things can change quickly. Gold posted double-digit gains for each of the past three years, more than doubling in price as central banks, asset managers and retail investors all piled into the trade. That rally ran out of steam in late January, shortly after the gold price hit an all-time-high near $5,600 an ounce. The stronger dollar and increased likelihood of interest rate increases make gold less attractive relative to yield-bearing assets. One bright spot for gold is the continued strength of central bank demand. Shares such as Implats, AngloGold, Goldfields, Implats and Valterra were all sharply down YTD.

Within industrials, shares such as Richemont, Anheuser-Busch and MTN produced good returns. However, this was mostly negated by disappointing performance from Prosus and Naspers, whose share prices have faced downward pressure this year of roughly 25% YTD. These two tech shares are still massively reliant on the performance of Tencent, which underperformed. In addition, their aggressive reinvestment plans/spending in its Brazilian food delivery unit, iFood, and the ongoing sale of non-core portfolio assets like Delivery Hero affected investor sentiment.

Banking shares such as Discovery, Standard Bank, Capitec and FirstRand have performed well this year as investors have become more optimistic about the outlook for the South African economy and the banks themselves continue to produce resilient earnings and deliver attractive dividends - combination of improving fundamentals and a re-rating of valuations. Property shares also boosted the financial sector, with the All Property Index up 10.5% in Q2.

The All Bond Index gained 7.8% after the SA 10-year bond yield dropped 70 basis points to 8.4% in Q2. Investors became more confident that local bonds offered value with improving fundamentals. The economy expanded more than expected in Q1 and recently received a credit rating upgrade from Fitch, following a similar action by Moody's in late May. Real yields from the local bond market remain attractive to foreign investors, with rigorous buying over the quarter.

Money market assets delivered a solid 1.7% in Q2 and 7% over the past 12 months.