A three-part series on the three pillars of risk profiling

Client risk-profiling has been construed as a rather controversial concept over the years but has gradually matured into a well-understood and matured, multi-dimensional process that is comprised of three key components: risk capacity (ability), risk required (need) and risk tolerance (willingness). In this, the first of a three-part series, we briefly recap each component to assist advisers and their clients, starting with risk capacity. Understanding the nuanced difference between the three pillars of risk profiling is vital for know-how investing.

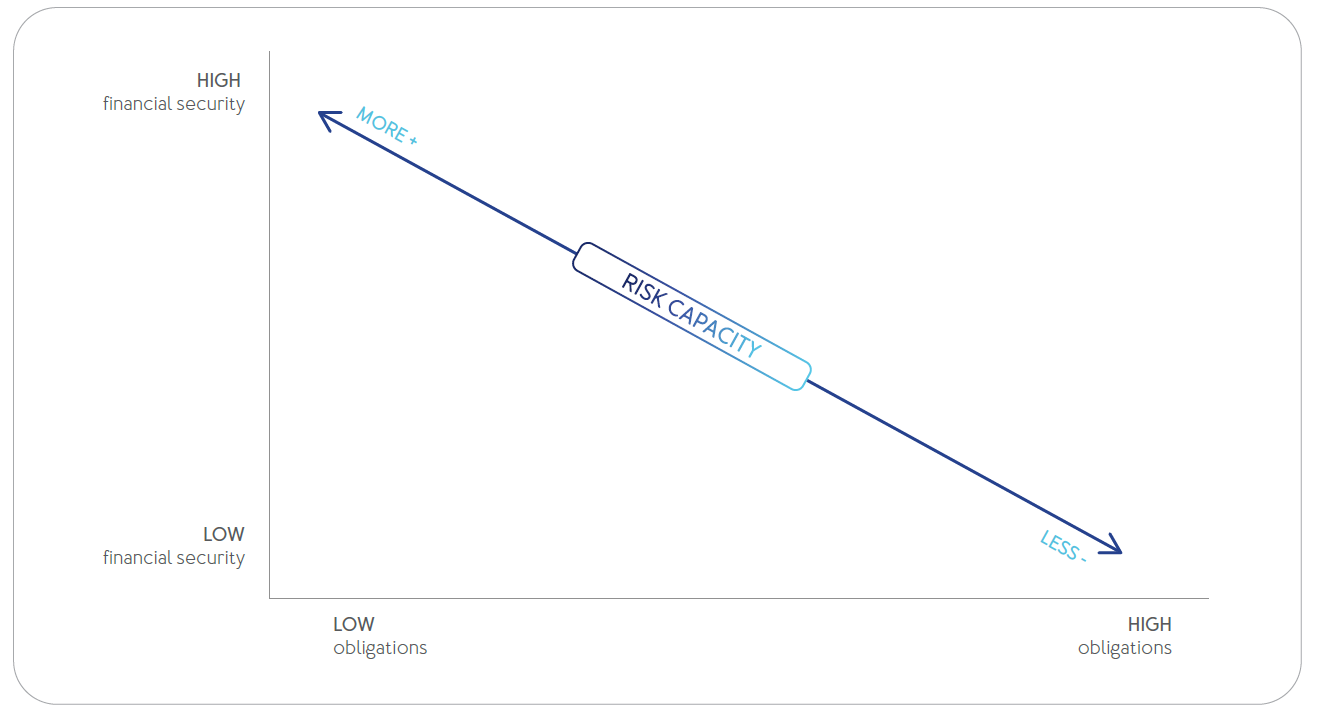

Assessing risk capacity is a cornerstone of holistic financial planning. A client’s capacity to take on risk refers to their financial ability to withstand losses without derailing their lifestyle or long-term goals. It is OBJECTIVE and MEASURABLE. Risk capacity is financial — how much loss you can sustain — and sets the essential boundary for a sustainable investment strategy.

The concept ties directly to real-world financial constraints and timelines. For example, someone planning to buy a home in the next two years generally has less flexibility to take on investment risk than someone with no major short-term financial commitments. Even if both investors feel comfortable with market volatility, their capacity to withstand losses may differ significantly. Risk capacity also considers whether someone can maintain their lifestyle or fulfill their obligations if their investments decline in value. It acts as a financial boundary that helps determine how aggressive or conservative a portfolio can realistically be. This boundary may shift over time with changes in income, expenses or life events, but remains rooted in financial realities rather than preferences or opinions.

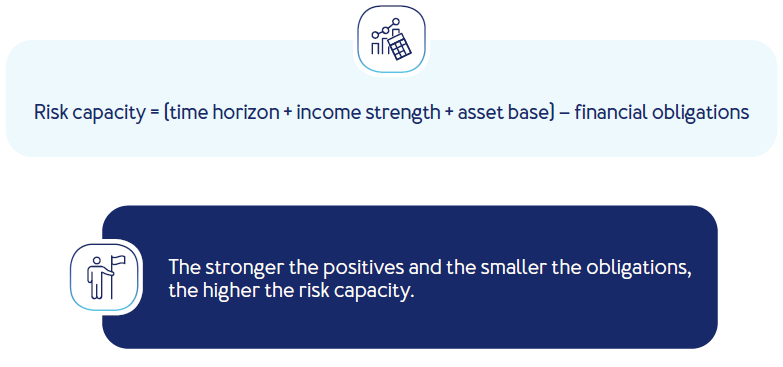

Risk capacity involves a combination of objective assessments:

Time horizon: longer time horizons allow for higher risk capacity because there is more time to recover from market downswings.

Income stability: stable, predictable income allows for greater risk-taking.

Liquidity needs: a high need for immediate cash (low liquidity) reduces capacity. Forced sales during a downturn are detrimental.

Financial obligations debt: high debt levels or imminent large expenses reduce the capacity to absorb losses.

Savings pot: disciplined savings over time compound in a meaningful investment/asset pool, allowing for greater risk-taking.

Measuring risk capacity involves analysing various aspects of a client’s financial life to determine how much investment risk they can realistically afford. It relies on quantifiable data and financial modeling, rather than subjective judgment.

The length of time before funds are needed plays a key role. A longer time horizon allows for a wider range of outcomes, giving more room for a portfolio to recover from market downturns. Someone investing for a goal 25 years away, generally has a higher risk capacity than someone needing access to their funds in three years’ time. Time horizon also influences how much liquidity and stability a portfolio may require. A portfolio that must generate income for living expenses or large upcoming purchases, has less room to absorb losses. Risk capacity drops when investors rely on their assets to fund near-term expenses, particularly if those expenses are fixed or unavoidable.

A steady or growing income stream can support a higher capacity for risk. And a high savings rate — asset base — can act as a cushion, helping replenish losses if markets decline.

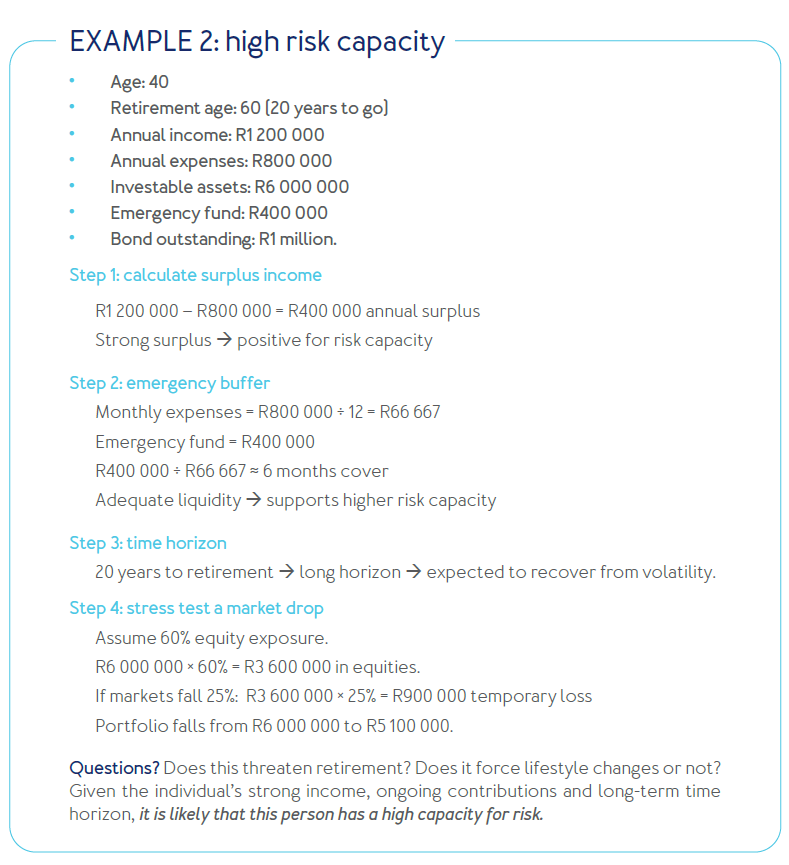

Imagine you are in your early 40s with a stable income and a sizable emergency fund, with retirement still 20 years away. You contribute regularly to investment accounts and have no large near-term expenses. In this case, it is likely that your financial situation supports a higher level of investment risk — you can afford to ride out market downturns because you will not need to access your portfolio soon.

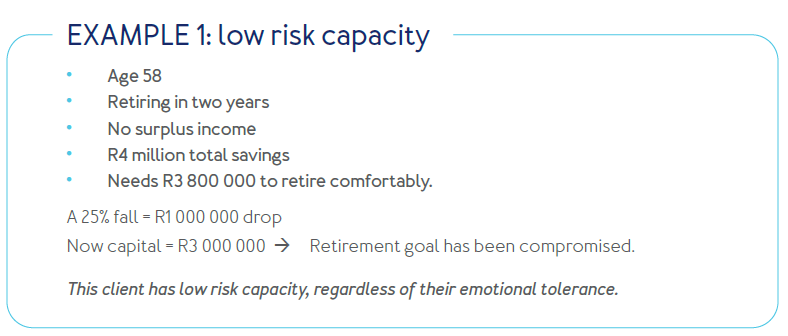

Now, picture a different phase of life: you are five years from retirement, helping a child through university and carrying a home loan. While your income may still be steady, the demands on your cash flow have increased and your time horizon has shortened. In this scenario, your risk capacity is likely to have decreased, even if your comfort with risk has not changed. These shifts show how risk capacity reflects your ability, not your willingness, to handle losses. It changes over time, depending on your life stage, financial goals and obligations. Recognising these shifts will help align your portfolio with your real financial situation.

The FAIS Act is very clear — advice must reflect a client’s financial circumstances and not just their appetite for risk. Hence, determining/calculating a client’s capacity for risk ensures compliance to the FAIS Act. It also prevents behavioural mistakes — clients who exceed their capacity are more likely to disinvest during market stress. Lastly, with risk capacity formulated, it strengthens the integrity of the client’s financial plan.

The bottom line is that the appropriate level of investment risk should never exceed a client’s financial capacity to withstand loss. It answers the question, “if markets fall by 20-30%, can I still achieve my goals without changing my plan?”

Risk is not something to avoid entirely but rather, something to manage intelligently. When risk capacity is clearly understood, expectations are realistic, portfolio volatility is easier to tolerate and emotional decision-making is reduced. Overall, it improves longterm investment discipline and ensures a financially sustainable investment strategy.