The second in a three-part series on the three pillars of risk profiling

Client risk profiling is a multi-dimensional process comprising of three key components: risk capacity (ability), risk required (need) and risk tolerance (willingness). In this, the second of a three-part series, we focus on risk required. Understanding the nuanced differencebetween the three pillars of risk profiling is vital for know-how investing.

|

Risk required refers to the level of investment risk a client needs to take to achieve their financial goals and objectives within a specific time frame. It answers the question: “how much risk MUST I take to realistically achieve my goal(s)?” If you have a high goal but low savings, your ‘required’ risk might be high, even if your ‘tolerance’ is low. It is different from risk tolerance (how much risk you can emotionally handle) and risk capacity (how much risk

you can afford to lose).

Every financial goal requires a certain return. For example, retiring comfortably, funding a child’s education or leaving a legacy. The core principle remains — the shorter the time horizon and the larger the goal relative to available capital, the higher the required return usually becomes. This is where mathematics meets reality. If you need a 10% annual return over 30 years to accumulate sufficient retirement funds, a conservative portfolio generating only 7% will not meet your requirements, regardless of how comfortable it feels. Risk required is particularly important because retirees are living longer, medical inflation remains high andclients often underestimate retirement capital needs. |

|

|

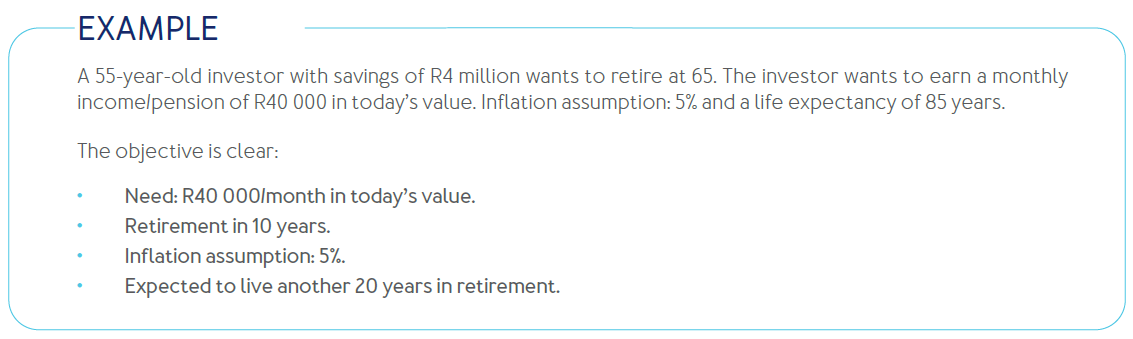

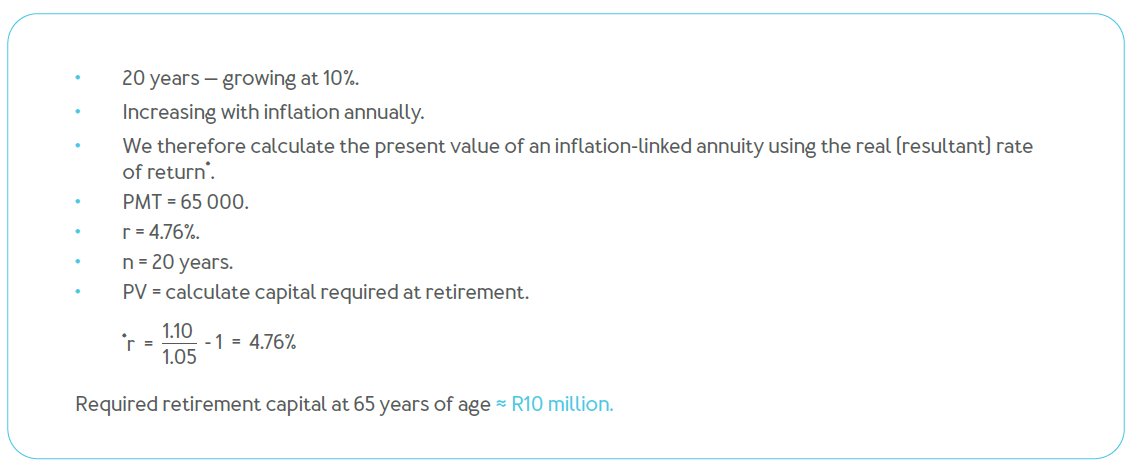

Required monthly income at retirement ≈ R65 000 per month (or around R780 000 per year |

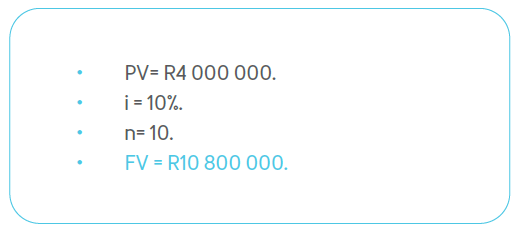

In this example, based on the current analysis and various assumptions, the client is on track and should achieve a surplus atretirement.

The client experienced a projected capital surplus at retirement because he diligently continued to invest in growth assets - a typical balanced and/or equity portfolio with a relatively high allocation to equities of 65% or more. The client alsoensured his investments were diversified between asset classes and asset managers.

The client is still 10 years from retirement, hence the need to continue investing in growth assets such as local and global equities. Including growth assets can improve long-term inflation-beating returns while also enhancing tax efficiency. Equity investments are often taxed as capital gains rather than as income. Annual capital gains exclusions can further assist in reducing overall tax exposure. The aim is to ensure that the client’s retirement objective ‘remains on track’, allowing the portfolio to grow sufficiently to combat inflation and support long-term income needs. |

|

|

Inflation risk (high medical costs), longevity risk (you may be fortunate enough to live another 20 years plus in retirement) and the fact that your compulsory annuity is taxed at your marginal tax rate, will mean that you need to continue investing in growth assets IN retirement. Your financial position when you eventually reti 65% to say 30%, but you would still need equity exposure. |

The gap analysis between a capital surplus or capital shortfall is one of the most important parts of financial/retirement planning and allows corrective action years before retirement. The risk required is not about what the client wants emotionally or what they prefer. When there is a shortfall, the planner must endeavor to reduce the gap through one or more corrective actions. On the other hand, if the goals are already achievable, excessive risk may no longer be necessary.

The most challenging scenario for a financial planner is to deal with a situation where a client has a capital shortfall and is simultaneously conservative i.e. has a low tolerance for risk/panics during volatility. The scenario may result in an unrealistic return need - risk required - but can be managed by the adviser exploring corrective options. For example:

In the case of a surplus the challenge is to protect accumulated wealth. It is imperative for the client to know - and understand - what needs to be done to reduce the risk of potentially falling into a shortfall. Hence, the importance of reviewing a client’s plan on a regularbasis remains key.

To recap, risk required is important because it:

The important principle is that risk required should never be assessed in isolation. Rather, it must be considered together with riskcapacity (as discussed in part 1 of this series) and risk tolerance. Thus, the most suitable financial plan is one where: