Article

Dear Wealth Manager, What’s In Your Tech Stack?

The client-driven demand for improved experience has prompted a digital transformation journey within the wealth management industry. This, combined with black swan events like the global COVID-19 pandemic, massive technological step-changes such as the rapid adoption of the metaverse, and advancements in regulation changes such as the pending introduction of RDR, shows just how critical digital transformation is to the survival of the wealth manager of the future.

The key to not only survive, but thrive, is through the deployment of technology across the advice practice.

A changed practice

It’s no longer about whether technology has changed the advice practice forever. We know it has. We are now at a stage where we want to know how effectively you, as an adviser, have embraced technology in order to remain relevant.

Advice practices can’t classify the adoption of tools and apps as a side of desk issue. You must give technology a central role in your advice offering. After all, if technology is effectively used, it has the power to become a competitive differentiator.

But what area of the business do you focus on for the greatest return on investment in both the short- and long-term? When there are so many providers and not a lot of integration, how do you navigate?

Where we currently stand

Enabling access to information that is real-time, relevant, and curated is critical to you, your clients, and your investment proposition. Data is prolific, even if effective insight into data is still somewhat elusive in the advice business.

Currently, the top trends in wealth management technology focus on three core areas:

- The adviser – covering support tech, AI, analytics, APIs and microservices.

- The client – including client-facing tech, conversational platforms, and the Internet of Things.

- The data – accounting platforms, cloud technology, process automation and blockchain.

What are some of the client and business demands driving the adoption of tech solutions and when these various applications are applied, what is the outcome?

By now, if you call yourself a wealth manager, you are most likely well-versed in the move to goals-based advice and how technology can support this . Tech adoption is no longer exclusively for the innovators; using technology in your business is simply a hygiene factor.

To get an idea of where you currently stand, start by auditing your existing systems, their utilisation, and the value they unlock for you. Consider if they are being used effectively and if increased utilisation in and of itself would unlock greater value for you and your practice.

Finding the missing pieces

It is important to consider your client’s experience throughout their journey with you. Acquiring new clients is much harder and more expensive than retaining and growing your existing client base. Retention, therefore, must be a priority in your business.

Bottom line: how do we leverage the data and insight we already have, to create exceptional client experiences that drive value and build loyalty?

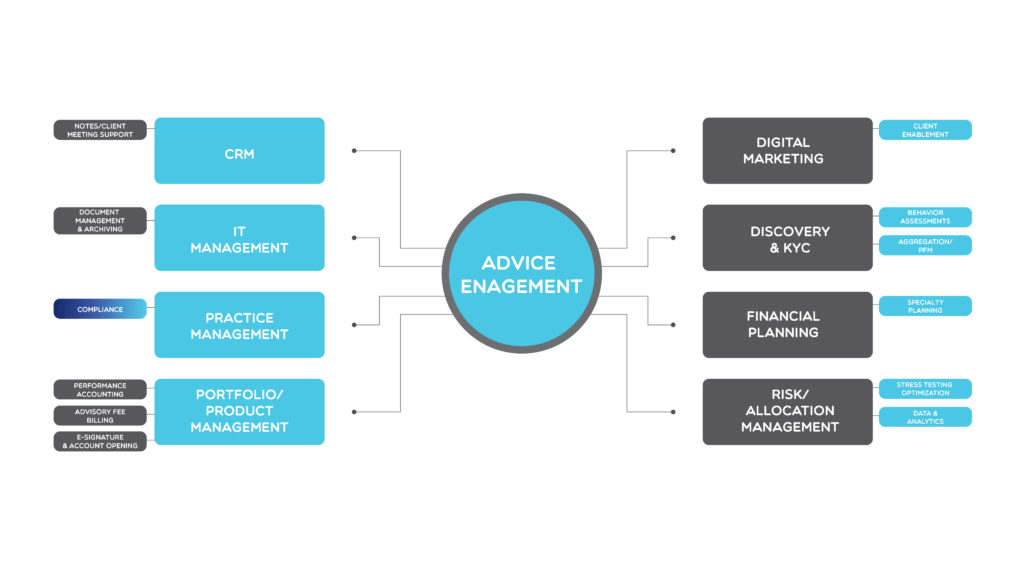

Armed with a tech audit of your business, the next step is to find the pieces of technology that will fill the gaps.

This wheel shows the categories of tech solutions and what efficiencies they consequently drive in the adviser business:

Source: Asset Map

Within each bucket, there’s a plethora of providers with the perfect solution for your business – or so they say. Rather than testing everything on offer, there are a few upfront considerations that will help you trim the list of potentials:

- Does it integrate into other systems you use or are planning on using?

- Is the data it produces clean and accurate and allows for simple manipulations?

- Is it too expensive or does its high cost perhaps directly result in a high ROI?

It’s the little things that count

While we can easily get caught up in figuring out the big issues, like the investment platform or CRM tool you have adopted or where you store all your files, there are two often overlooked areas that will really make the difference.

Let’s get hyper personal

Highly customised service with tailored feedback has long since been a driver of loyalty in the retail industry – think of when you open Netflix or Spotify. Clients expect the same level of intuitive personalisation from their financial adviser.

In the 2019 Temenos and Forbes Insights survey of wealth-management executives, an overwhelming 82% of respondents believed that those who increase product personalisation will succeed.

And there’s a reason: Exceptional customer experience drives loyalty. Remembering a birthday or that your client requested that you check in on a specific date about a decision they had made makes all the difference and becomes a strong brand differentiator.

Yet the lack of time and the challenge of juggling an already heavy workload makes this level of personalisation seem completely insurmountable.

That’s why organizations need to invest now in the data, analytics, and AI initiatives that will help them to offer targeted advice, follow ups and follow-throughs that help provide coveted hyper-personalised experiences for their clients.

Hack, yes!

Most organisations can be hacked within half an hour, despite promises from chief executives they take cybersecurity seriously. This is according to cybersecurity specialist Michael Connory.

The breadth and depth of personal information that advisers retain should make even the bravest of us nervous. As an adviser, it should actually be causing you sleepless nights – the financial, legal, and reputational impact can be significant.

So, what are you doing about securing your data? While there’s a perception that it is a highly sophisticated, highly complex and highly technical area – and in some cases this is true – in most cases it is about covering the basics. For example, password hygiene: change regularly, make them long and complex, use two-factor authentication where possible, don’t use the same across multiple applications.

If you put in place the basic hygiene elements – which are free ! – you’re going to put yourself in a much better position to protect yourself, your business and, most importantly, your clients, against this threat.

And yes, even your email has data!

The final word

As a wealth manager of the future, technology, and the use of it in your practice, must be integral to your business strategy – it’s the key to scalable growth.

How do you eat an elephant? One bite at a time and that is the best way to drive technology step change in your advice practice.