Article

The UK’s Consumer Duty: How relevant is it to South African firms?

The last fourteen years have seen official regulatory reform, but perhaps more impressive, significant strides have been made through self-regulation and industry-led initiatives.

Back in 2011, National Treasury released its policy document for a more inclusionary financial system under the title: “A safer financial sector to serve South Africa better”. The document included the separation of prudential and market conduct regulation and identified the following policy priorities:

- financial stability,

- consumer protection and market conduct,

- expanding access through financial inclusion, and

- combating financial crime as key to building a financial sector which is safe and serves all South Africans.

In line with these principles, the regulatory framework for the financial sector is structured around the Twin Peaks model, which delineates oversight responsibilities between two primary bodies. The Prudential Authority oversees the stability and health of financial institutions, ensuring they are secure and sound. Concurrently, the Financial Sector Conduct Authority (FSCA) is tasked with overseeing market conduct, ensuring that financial entities operate with integrity and transparency.

In that same year, 2011, the Financial Services Board, the FSCA’s predecessor, published the Treating Customers Fairly (TCF) Roadmap, which eventually formed the basis of the policy framework, which has six principles and takes an outcomes-based regulatory and supervisory approach. Financial institutions are obligated to fulfil specific objectives in their compliance with the TCF mandates.

Since then, many acronyms have been the flavour of the year, with RDR (Retail Distribution Review) eliciting healthy debate and responses until it was announced last year that these reforms will now be mixed in with the CoFI (the Conduct of Financial Institutions) Bill. And as South Africa’s most contested democratic election year rolls around, the promulgation date for CoFi is still uncertain.

While the industry might still be waiting for the official legislation to be approved, stakeholders have not been resting on their laurels.

“It has been encouraging to see how advisers in South Africa proactively embraced these governance principles in their daily operations and implemented them without legislative obligation.”

The global influence

South Africa’s financial services sector does not operate in a silo, isolated from the rest of the world. The naming convention of the regulatory pieces is a case in point. RDR stems from the Retail Distribution Review that happened in the UK, CoFi is also the name of the Act in New Zealand that amends the Financial Markets Conduct Act of 2013 in that jurisdiction and TCF is an outcomes-based regulatory and supervisory approach well-known in Europe.

And so, on 31 July 2023, the UK’s Financial Conduct Authority’s Consumer Duty came into force for existing products and services offered. Some players have described it as “one of the biggest shake-ups to retail financial services regulation” and South African financial services providers will be best served to keep an eye on the developments and prepare themselves proactively.

A seismic shift

According to the UK’s FCA, the duty means that consumers should get:

- the support they need, when they need it

- communications they can understand

- products and services that meet their needs and offer fair value

The FCA also, very firmly, issues a warning that it will closely monitor how firms are putting these new rules in place and that it will “take action” against those that aren’t following them.

A Grant Thornton article discussing the objectives of Consumer Duty highlights a shift in focus. Where the priority once was on fair treatment of customers and preventing negative outcomes, businesses are now expected to proactively ensure positive outcomes for their clients. This change might appear to be merely theoretical, but it necessitates a substantial shift in corporate culture and the adoption of new practices that prioritize the customer’s interests. This transformation goes beyond merely revising policies and procedures; it involves a fundamental alteration in a company’s operational approach.

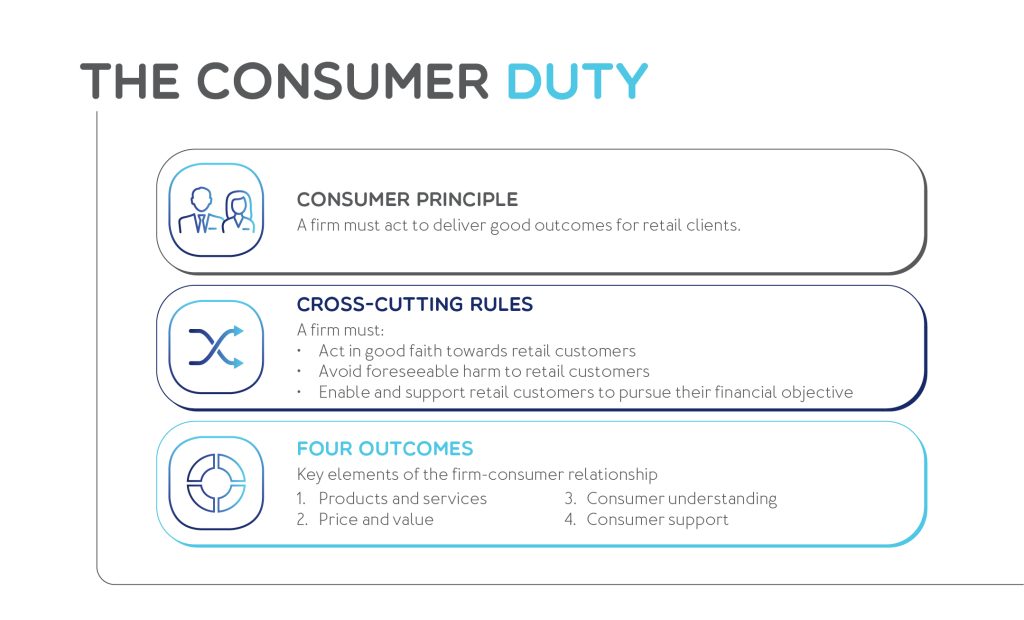

The following KPMG illustration shows the three components that essentially comprise the new Consumer Duty.

A key aspect of Consumer Duty is that firms monitor and demonstrate that they are acting to deliver good customer outcomes. But what does that mean in practice?

When it comes to financial performance and planning, markets are volatile, and returns will vary over time. It can therefore not always mean a better-than-expected growth outcome, can it?

As highlighted in the diagram above, there are four outcomes which should be achieved.

Consumer understanding: FSPs in the UK must now ensure consumers are equipped to make good decisions, with access to understandable and timely information. In their advisory practice, advisers would have to make sure the communication they send out is tailored for the audience and likely to be understood by the client, and that it can then equip them to make decisions that are effective, timely and properly informed. They should also test, monitor, and adapt communication to support understanding.

Products and services: This outcome aims to improve product design and clarity so that it meets the needs of the clients who purchase it. It also asks that the intended distribution strategy for the product or service is appropriate for the target market and requires the FSP to conduct regular reviews to ensure compliance.

FSPs in the UK are increasingly being asked to ground their strategy in evaluating how well their products and services meet the audience’s needs, demonstrating the value proposition. They should rank and assess their offerings based on risk, then outline necessary enhancements with designated overseers.

Price and value: When looking at this outcome the UK FSP or adviser, should ask if there are any elements of the pricing structure that could lead to harm and if fees and charges appear unjustifiably high compared to the benefits of a specific product or comparable products.

Consumer support: The FCA expects FSPs in the UK to design and deliver support that meets the needs of customers. They should also ensure that customers can use their products as reasonably anticipated. Interestingly, one article highlights that they should include “appropriate friction in customer journeys to mitigate the risk of harm and give customers sufficient opportunity to understand and assess their options, including any risks”. But, at the same time, make sure that customers do not face unreasonable barriers during the lifecycle of a product or service.

What does this mean for South African advisory services?

The four outcomes of Consumer Duty may seem familiar; their essence can be found expressed in different ways in existing South African legislation, codes of conduct or industry standards. While there may not be any significant new requirements per se contained in UK Consumer Duty, the important change is one of posture. The UK legislation seeks to orient and mandate FSPs around ‘proactive positive’ client outcomes (i.e. more than simply preventing negative ones). South African financial services providers and wealth advisers should take heed of the UK’s Consumer Duty regulation and how its implementation plays out. The financial sector is increasingly interconnected globally and as regulations evolve in major financial centres like the UK, they have in the past, set the example for other regulators globally. Understanding and pre-emptively adapting to these changes can give South African firms a strategic advantage.

If you want to learn more about the intricacies of the legislative and regulatory changes in South Africa, listen to our podcast on the topic here.

By observing and integrating elements of the UK’s Consumer Duty regulation, South African financial advisory players can enhance their service quality, mitigate regulatory risks, and position themselves as forward-thinking and proactively client-positive in a competitive market.